Forecasting holiday sales and performance is tricky. One needs to infer conclusions by, say, mid-summer at the latest, then wait six months or so to verify one’s accuracy.

Instead, let’s take a look back. Let’s compare 2023 narratives to their 2024 realities. From this, we should be able to glean insights regarding the upcoming holiday season. From extended shopping timelines to strategic discounts to consumer debt, there are plenty of topics well situated to impact the holiday season.

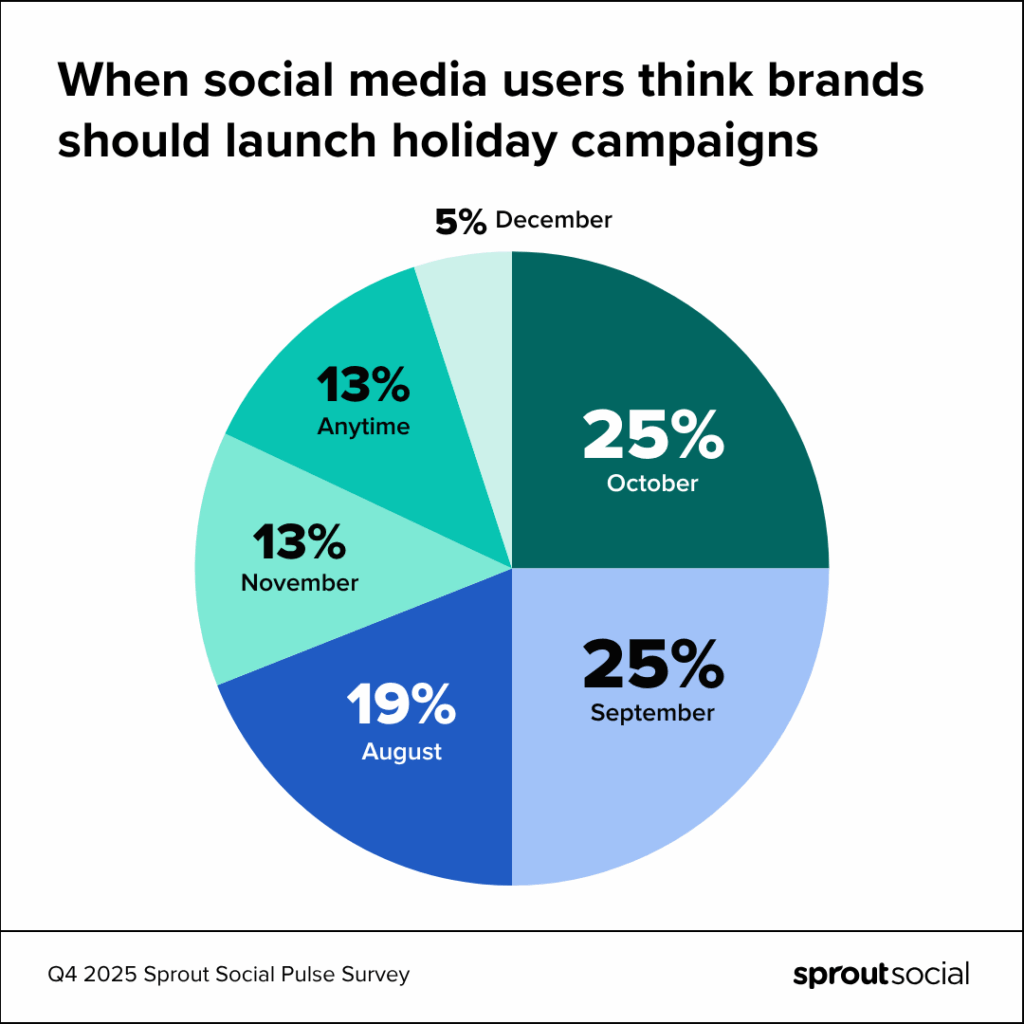

Winter Holiday Shopping Keeps Starting Earlier

It’s no surprise that the Winter Holidays seem to keep creeping earlier and earlier, with some even joking that Halloween is the only thing keeping us from hearing Mariah Carey on July 4th. But even if retail stores don’t switch from spooky season to something more festive until closer to November, that won’t stop consumers from shopping.

2023 Narrative

According to Ipsos, 19% of consumers planned on beginning their holiday shopping in October.

2024 Reality

By 2024, that number had increased to 25%.

What to expect in 2025

Look for the season to keep getting pushed back. This is for several reasons. The first is simply a matter of budgeting. Tight paychecks and increasing holiday expectations create a pinch for consumers, one that can be navigated with longer planning sessions and earlier spending. $500 paid off over four months is a lot easier than $500 paid off over four weeks.

This larger runway also creates additional discount opportunities. Pre-Black Friday sales and other promotions could get customers in the door nice and early – while their budget is still fresh and healthy.

Look for the sales cycle to keep extending, as 44% of Sprout Social survey respondents think holiday campaigns should begin before October and 1 in 5 believe campaigns should start in August.

{kind=link}

Discounts Keep Getting Steeper

Discounts are a pure quality-for-quantity play. It involves the brand slicing off a bit of profit margin to increase sales volume. Used appropriately, they can be a total game-changer for a retailer. But when every brand is using them, it doesn’t become a special event – it becomes the norm.

2023 Narrative

Predictions were that certain brand segments (e.g., luxury) would be foregoing discounts in favor of other perks and savings, such as free shipping, gift wrapping, and even early access to special products.

2024 Reality

Discounts were still very much a thing. Fiserv reports that same-store sales were up 4.1%, and transitions up 5.4%. But – average ticket size was -1.1%.

What to expect in 2025

The fact is, discounts around the holidays aren’t the special events they once were. They’re table stakes now. Rather than giving a brand a distinct advantage, it instead invites competitors to join a race to the bottom. Theoretically, the consumer wins in this case. But overwhelmed by solicitations and non-stop, hyper-targeted ads, shoppers are being crushed under the noise.

Consumer Debt Was Down 14%. This is very bad.

A surprising subhead, until you drill down to the nitty gritty.

2023 Narrative

50% of consumers were expected to take on holiday debt. This had a lot of concerning implications. People simply can’t pay for the holidays the way they used to, so they were planning to borrow to make a perfect day for their family. The net result is they ended up repaying it – with interest – over months. It’s not an impossible thought that some consumers may be paying off last year’s debt while beginning the cycle anew.

2024 Reality

Holiday debt was down to just 36%. At first blush, this sounds like a huge relief. It suggests that consumers weren’t as stressed or cash-strapped as they appeared to be.

The reality is much worse.

The 50% quoted above refers to people who take on debt specifically for holiday shopping. It doesn’t include people entering the holiday season who were already carrying debt, nor does it include Buy Now, Pay Later (BNPL) services. At the time of this writing, BNPL is not reported as debt. It looks like debt. It smells like debt. But it’s not reported as debt.

That means the 36% doesn’t account for a lot of hidden numbers. And those numbers are alarming.

Total consumer debt climbed from $17.15 trillion in 2023 to $18.39 trillion in 2025. Meanwhile, BNPL sales were $80 billion in 2023, and are expected to hit $97 billion in 2025.

However – because BNPL isn’t classified as “debt,” its users are racking up unsecured death-by-a-thousand-cuts microloans that don’t seem like a big deal. Until someone has 5 payments. 10. 20. At that point, the economic pressures begin to make the ghost of Christmas shopping past a thing that could put increasing pressure on shoppers well into 2026.

Final Outlook

Shopping seasons are starting earlier, discounts are getting bigger, and consumers are going deeper and deeper into debt to meet the increasing social demands of a perfect winter holiday.

This paints a picture of a market built on quicksand. Unless we see some critical social changes, expect the same going forward—more debt, more discounts, and less consumer relief than ever.